FY24/25 in Review and What Lies Ahead

Before we assess the market environment retrospectively, we considered our prospective view of how FY 24/25 might unfold - published in July 2024.

Outlook for FY24/25

“………. we can only evaluate what might happen in the coming year with the information at our disposal today.

The known knowns are already factored into market prices – as these are always forward looking. These are:

- Trump will likely win the US election, and his de-regulation and reduced taxes policies are likely good for company earnings – in the short term.

- Decreased US taxes will add to an already problematic US fiscal debt and deficit problem – but markets are not presently concerned.

- Trump’s tariff policies are inherently inflationary – especially if these provoke retaliatory tariffs by other countries.

- The global economy – while slowing – remains strong and the company earnings outlook is positive.

- Shares – especially US and large tech company shares – are expensive.

- Expected future returns are a function of the starting point. Where the starting point is at a high – expected returns are lower than they would have been had the starting point been at a low.

The known unknowns include:

- To what extent might a second Trump presidency spell the end of the Pax Americana, or the Rules-based order?

- The Middle East situation.

- Whether the US elections deliver a clean sweep of the Presidency, the House and the Senate to the Republicans.

- The impact of AI on productivity.

- When / if markets will impose discipline on profligate governments globally.

Looking forward at the next 12 months [i.e. the 2024/25 financial year] and based on current market prices, we would expect muted share market returns, and good single digit returns in excess of bank deposit interest – from high credit quality, fixed and floating interest securities.

- There is a probability of high levels of volatility associated with equity prices – as any disappointing inflation / growth / unemployment reading may undermine market confidence significantly.

- And longer duration fixed interest securities may disappoint – if: US: tariff policy comes to fruition / is more extreme than anticipated / provokes retaliation; or the market finally no longer accepts continuing expansion of debt and deficits and adds a risk premium (higher yield requirement) to US treasuries.

What happened in FY24/25?

In Brief:

- 2024–25 delivered another year of good returns notwithstanding high levels of volatility associated with elevated asset prices, geo-political tensions, US tariffs and recession fears, the US bombing Iran, elevated government debt levels, and an unsustainable US government debt trajectory.

- Good returns have been supported by central bank interest rate reductions, and economic growth proving more resilient than expected.

In this environment of elevated asset prices and highly elevated levels of uncertainty:

- Professional investors – exercised caution (as we have)

- Retail investors – kept ‘buying the dip’

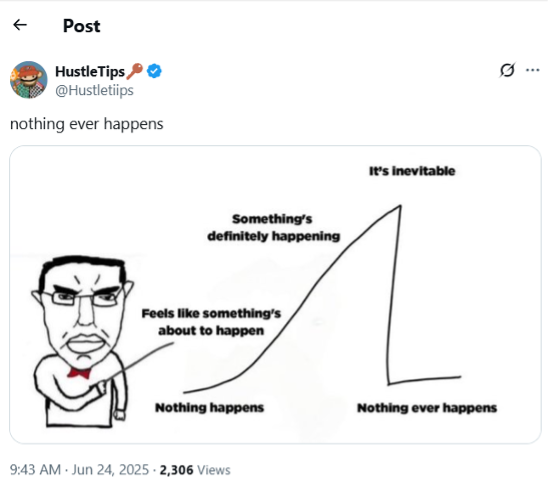

The Economist published an article on June the 18th which is consistent with our investment philosophy – and a timely reminder of what it’s all about.

“Investors ignore world-changing news. Rightly

The Nothing Ever Happens Market

Missile warfare has erupted in the Middle East. On June 13th, as the bombs began to fly, S&P 500 futures fell by 1.6%. But as the hours passed, the stockmarket steadily climbed. The index has now recovered to around 6,000, a hair’s breadth from an all-time high. Such movements reflect a new market mantra: ‘Nothing ever happens.’ The phrase emerged from the depths of 4chan, an online forum, more than a decade ago, and has become a popular meme among youngish investors. On the face of it, the saying seems wildly out of place in an era of both trade war and conventional conflict. But consider the long list of recent events that at first seemed to have epoch-making potential, only to fizzle out, and it appears more reasonable.”

“…..And so, cynicism prevails, dips are bought, and markets continue to climb. Retail investors are getting in on the act, too. They have piled into stocks, buying $20bn-worth, net, over the past three months. Crisis, what crisis?

The head-in-the-sand approach is a more sophisticated strategy than it first appears, and not just because headlines tend to go over the top.”

The article goes on to observe various studies on what really moves the stockmarket.

“….almost five decades of world-changing events, from Japan’s attack on Pearl Harbour in 1941 and the Cuban missile crisis of 1962 to the Chernobyl nuclear meltdown in 1986. They were surprised to discover that the volatility of returns (as measured by the standard deviation) on the day of an important news event was less than three times as large as on an ordinary day. Several of the biggest one-day falls identified by the authors occurred on days without an obvious news-related spark.”

The Economist observed that (our emphasis):

“The momentum of markets can be relentless. Shares tend to grind higher over time as consumers spend, entrepreneurs innovate, and companies grow. Earnings per share for American firms have risen by 250% or so over the past 15 years. For any event to have a meaningful impact, at least for longer than a few days, it must harm such dynamism.”

We have constantly and almost boringly emphasised that “as long as capitalism survives” investments in shares – will over the longer term – earn a superior return to that of cash.

As managers of your money, we do not take the above as license to speculate and “go all-in”.

Our core responsibility to you is to ensure we support you in the achievement of your goals and objectives. So, we take no more, nor no less risk – than is necessary to achieve your objectives.

As The Economist notes in its conclusion (our emphasis):

“Of course, an event of sufficient scale to rattle markets may be on the way*. That would upset the dip-buyers. But what appears to be a witless stampede into stocks, even in moments of international tension and conflict, is really an appreciation of the power of capitalism. The news that matters, tends to come from the real economy or financial system—not the world’s battlefields.”

- AFR: Viktor Shvets on the risks markets aren’t seeing

Our outlook for 2025/2026:

The known knowns are already factored into market prices – as these are always forward looking. These are:

- Tariffs will end up considerably higher than might have been expected. They are a strategic revenue raising requirement to fund the Federal Deficit.

- Tariffs are inflationary and reduce consumer spending.

- Inflation upside limits interest rate reductions.

- The US Federal Deficit is unsustainable and exacerbated by the One Big Beautiful Bill.

- The market will impose its discipline. We just don’t know when.

- The impact of decreased US taxes is on the margin – as the Bill largely extends tax reductions that were about to expire. The impact on economic growth will likely be marginal.

- Money is leaving the US – reflected in a declining dollar.

- Europe is delivering material financial stimulus.

- The global economy appears to be resilient.

- Share valuations are elevated.

- Company earnings must deliver in order to support these valuations.

- Expected returns must be lower than historical – as a consequence of a high starting point.

- Returns on interest bearing securities are reducing but remain attractive relative to shares.

- There is significant uncertainty regarding the full faith and store of the USD, and significant US political uncertainty. Gold is one haven.

- The US mid term elections are next year. US politicians will be incentivised to deliver good news, financially.

The known unknowns include:

- The Middle East situation.

- China and Taiwan.

- Russia and Ukraine / Europe.

- The final level of and impact of Tariffs.

- The impact of mass deportations of immigrants from the US on US wages – and inflation.

- The impact of AI on productivity and unemployment.

- When / if markets will impose discipline on profligate governments globally.

So, for the coming financial year:

- Expect ongoing volatility – as the market digests the implications of The One Big Beautiful Bill, the end of the 90 day tariff pause, Iran’s response to recent events, Russia digging in against Trump in Ukraine, and the possibility of weaker growth and company profits.

- Moderate your return expectations:

- Factually: we have had 3 consecutive years of 8%+ returns on growth portfolios; share market valuations in the US and Australia are elevated, US government debt is unsustainable, tariffs are inherently inflationary, reducing consumption and company profits – while limiting interest rate reductions. Geopolitical risk remains high.

- Those brave enough to forecast returns for FY 2025/26 suggest growth portfolios with 70–80% in growth or risk asset may deliver <8% returns*.

- Shane Oliver (AMP) – Investment outlook

%201.svg)